Guidance on Zero-Rated and exempt supplies

Value-Added Tax or VAT is a tax on the consumption or use of goods and services levied at the point of sale. VAT is a form of indirect tax and is used in more than 180 countries around the world.

The government of UAE published guidance on zero-rated and exempt supplies on their website (government.ae).

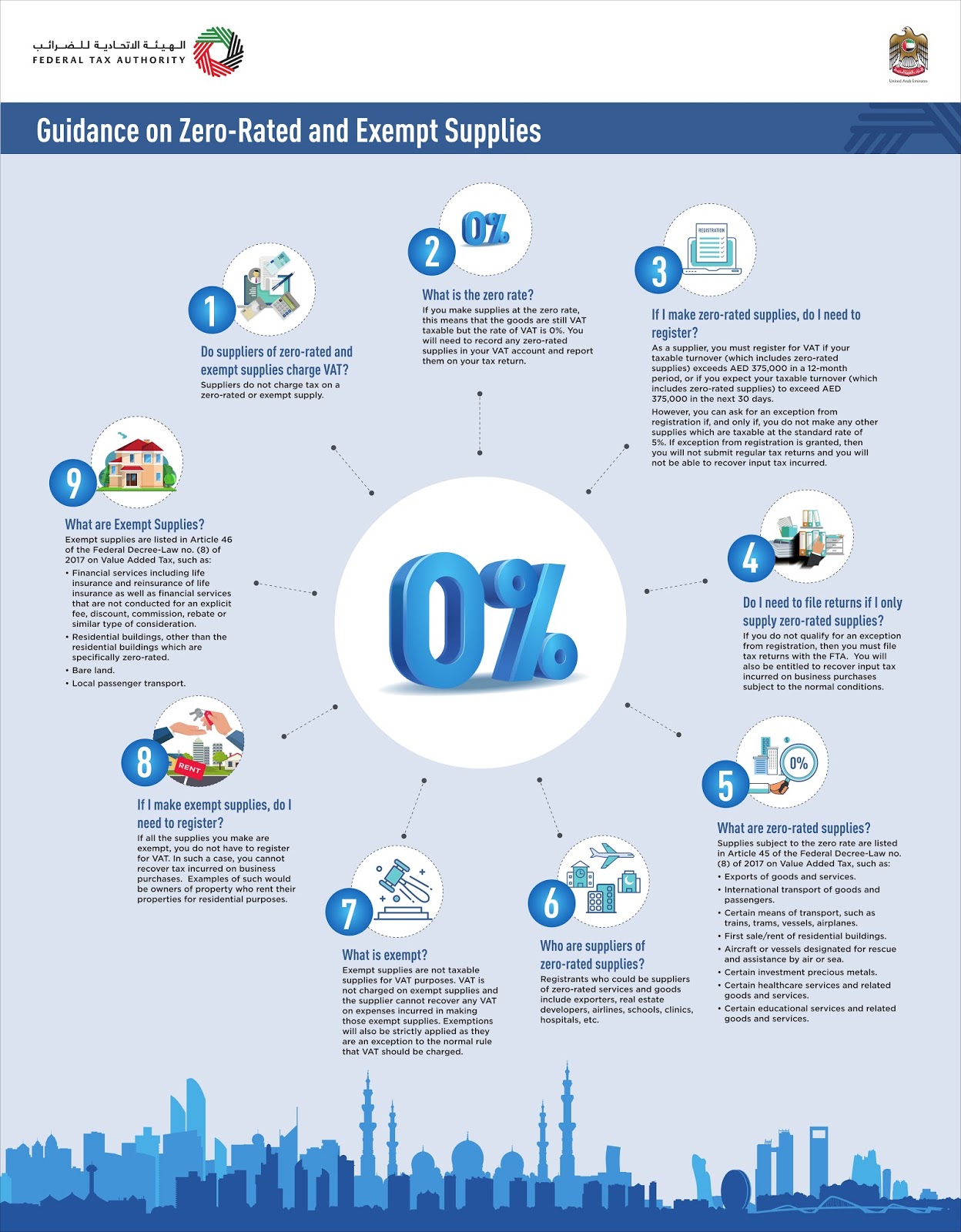

Q.1: Do suppliers of zero-rated and exempt supplies charge VAT?

Suppliers do not charge tax on a zero-rated or exempt supply.

Q.2: What is the zero rate?

If you make supplies at the zero rate, this means that the goods are still VAT taxable but the rate of VAT is 0%. You will need to record any zero-rated supplies in your VAT account and report them on your tax return.

Q.3: If I make zero-rated supplies, do I need to register?

As a supplier, you must register for VAT if your taxable turnover (which includes zero-rated supplies) exceeds AED 375,000 in a 12-month period, or if you expect your taxable turnover (which includes zero-rated supplies) to exceed AED 375,000 in the next 30 days.

However, you can ask for an exception from registration if, and only if, you do not make any other supplies which are taxable at the standard rate of 5%. If exception from registration is granted, then you will not submit regular tax returns and you will not be able to recover input tax incurred.

Q.4: Do I need to file returns if I only supply zero-rated supplies?

If you do not qualify for an exception from registration, then you must file tax returns with the FTA. You will also be entitled to recover input tax incurred on business purchases subject to the normal conditions.

Q.5: What are zero-rated supplies?

Supplies subject to the zero rate are listed in Article 45 of the Federal Decree-Law no. (8) of 2017 on Value Added Tax, such as:

- Exports of goods and services.

- International transport of goods and passengers.

- Certain means of transport, such as trains, trams, vessels, airplanes.

- First sale/rent of residential buildings.

- Aircraft or vessels designated for rescue and assistance by air or sea.

- Certain investment precious metals.

- Certain health care services and related goods and services.

- Certain educational services and related goods and services.

Q.6: Who are suppliers of zero-rated supplies?

Registrants who could be suppliers of zero-rated services and goods include exporters, real estate developers, airlines, schools, clinics, hospitals, etc.

Q.7: What is exempt?

Exempt supplies are not taxable supplies for VAT purposes. VAT is not charged on exempt supplies and the supplier cannot recover any VAT on expenses incurred in making those exempt supplies. Exemptions will also be strictly applied as they are an exception to the normal rule that VAT should be charged.

Q.8: If I make exempt supplies, do I need to register?

If all the supplies you make are exempt, you do not have to register for VAT. In such a case, you cannot recover tax incurred on business purchases. Examples of such would be owners of property who rent their properties for residential purposes.

Q.9: What are Exempt Supplies?

Exempt supplies are listed in Article 46 of the Federal Decree-Law no. (8) of 2017 on Value Added Tax, such as:

- Financial services including life insurance and reinsurance of life insurance as well as financial services that are not conducted for an explicit fee, discount, commission, rebate or similar type of consideration.

- Residential buildings, other than the residential buildings which are specifically zero-rated.

- Bare land.

- Local passenger transport.

Very helpful guide! Understanding zero-rated and exempt supplies is crucial for businesses operating in the UAE to ensure accurate VAT compliance and avoid penalties. Correctly identifying which supplies fall under these categories can streamline accounting and reporting. Partnering with experienced VAT consultants in Dubai can provide the necessary guidance to manage VAT efficiently and stay fully compliant with the UAE tax regulations.

ReplyDelete